The accounts receivable function is the lifeblood of a business.

Businesses depend on the cash received and posted by accounts receivable departments for:

![]() The purchase of raw materials

The purchase of raw materials

![]() Sales and marketing

Sales and marketing

![]() Research and development

Research and development

![]() The manufacturing and delivery of goods

The manufacturing and delivery of goods

![]() Payroll and administration

Payroll and administration

But processing and applying customer payments is easier said than done for most businesses.

The root of the problem is the manual processes on which most receivables departments rely.

Most businesses have not fully automated their payments processing and accounts receivable. Many have a mix of manual processes and loosely integrated payments and cash application systems.

As a result, 57% of businesses manually apply most of the payments that they receive, Aite Group reports.

Worse, 30% of businesses cannot apply any of the payments they receive without human operator intervention.

Aite Group research finds that only 13% of remittance data arrives in a format that can be automatically ingested by legacy accounts receivable systems.

The result is lots of keying.

Moreover, applying customer payments is so complex that 20% of businesses lose more than $250,000 annually to unauthorized deductions that cannot be resolved.

Manual processes and loosely integrated systems also make it hard for receivables departments to achieve treasury connectivity. Businesses can never be sure where things stand with their cash.

Accounts Receivable Departments Puzzle

The growth of electronic payments is making things worse for accounts receivable departments:

![]() Businesses frequently receive electronic payments such as ACH transactions that are decoupled from their remittance advice, which are typically e-mailed as a PDF attachment, Word document or an Excel spreadsheet or embedded in the body of an e-mail.

Businesses frequently receive electronic payments such as ACH transactions that are decoupled from their remittance advice, which are typically e-mailed as a PDF attachment, Word document or an Excel spreadsheet or embedded in the body of an e-mail.

![]() The lack of U.S. remittance standards means that billers can never be sure what format they will receive remittance data from customers – or if they will receive any data at all.

The lack of U.S. remittance standards means that billers can never be sure what format they will receive remittance data from customers – or if they will receive any data at all.

![]() Even in cases where customers are willing to transmit remittance data as part of an ACH payment record, the lack of U.S. remittance standards requires a biller’s time-strapped IT department to map the data for import or receivables departments to key the data.

Even in cases where customers are willing to transmit remittance data as part of an ACH payment record, the lack of U.S. remittance standards requires a biller’s time-strapped IT department to map the data for import or receivables departments to key the data.

![]() Bank lockbox providers use different file formats for transmitting remittance data to billers, requiring a biller’s IT department to map the data for import or to key the data.

Bank lockbox providers use different file formats for transmitting remittance data to billers, requiring a biller’s IT department to map the data for import or to key the data.

Receivables departments have better things to do than spend all their time on low-value tasks such as manual data entry, hunting down remittances, resolving exceptions and posting receivables. This is especially true in today’s turbulent economy, where receivable departments should be focused on strategic activities such as data analysis, working capital optimization, and customer management.

Deploying another standalone system won’t help.

THE SOLUTION

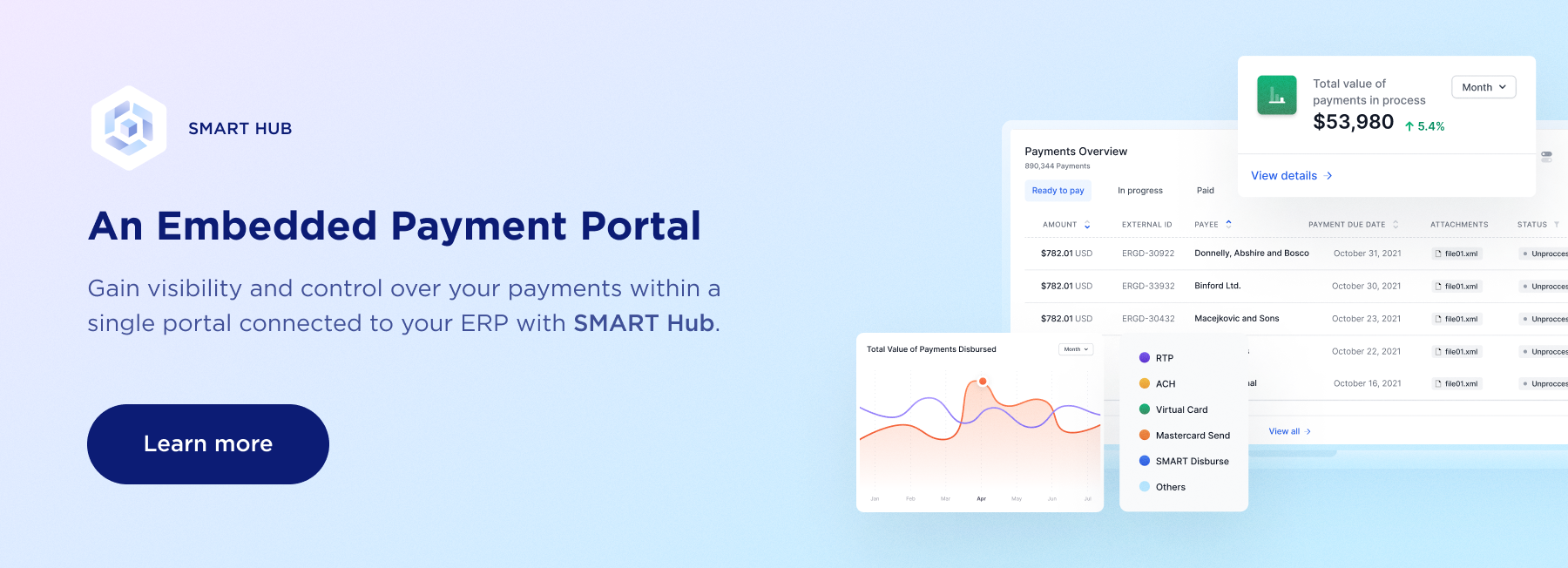

Embedding payment capabilities into legacy software and ERP platforms so payments and rich remittance details can electronically flow fast, accurately, and touch-free.

Does Your Receivables Department Need to Automate?

Here are five tell-tale signs that it’s time to automate your accounts receivable processes:

.png?width=30&height=30&name=1%20(2).png) You Have Lots of Manual Processes

You Have Lots of Manual Processes

In most businesses, matching payments with remittance advices is a manual and increasingly complex affair. The root of the problem is that there are no standards for remittance advices in the United States. The data on remittance advices is frequently inaccurate, incomplete and hard to find – if the customer sends it all.

Businesses also receive multiple remittance file formats from bank lockbox providers. And most accounts receivable departments cannot access the IT resources that they need to map the remittance data in bank files and ACH payment records for import into their legacy systems.

Your Costs Are High

Your Costs Are High

Businesses spend more than $100 billion annually on their receivables processes, studies show. Much of that money is wrapped up in the human labor required to process and match payments and remittance advices. Some businesses pay bank lockbox providers enormous fees (as much as $50,000 a month, in some cases) to process their customer payments and to capture or key the data from remittance advices.

Unfortunately, the data provided by banks can be so unreliable that most businesses apply a puny percentage of their electronic payments straight-through to their ERP application or system of record.

You Have Lots of Unapplied Cash

You Have Lots of Unapplied Cash

Ineffective posting of payments and remittance advices results in a high amount of unapplied cash (money that’s held in a general account while the business tries to determine how the funds should be applied to customer invoices). Beyond the potential customer service implications of not applying a payment correctly or in a timely manner, unapplied cash can also create complex escheatment issues in many states.

You Have Customer Service Issues

You Have Customer Service Issues

Poor cash application opens the door to customer issues such as lots of inquiries regarding payment status, erroneous collections activity, delayed shipments (think: just-in-time deliveries) and unnecessary credit holds (which can result in customers taking their business elsewhere while you determine how to apply their payment).

You Do Business Internationally

You Do Business Internationally

Global businesses - which may have financial shared services facilities across several continents - must manage numerous banks and currencies, multiple ERP applications and divisions (with potentially complex parent/child relationships), and various file formats and payment methods (e.g. EDI 820, MT 940 and MT 942, BACS, RIBA and SEPA). Making matters worse, it is not customary to send a remittance advice in the United Kingdom and other countries in Europe.

If your business is experiencing any of these issues, you have no time to waste in automating.

Time to Automate Payments Processes

Seventy-one percent of accounts payable departments plan to make more payments to suppliers electronically because of the operational disruption caused by the pandemic. Even 44% of accounts payable departments that describe themselves as “largely automated” plan to deploy more technology for paying suppliers electronically.

This means that receivables departments can anticipate receiving a lot more electronic payments and electronic remittances from customers. Departments with manual processes will need to find more efficient ways to handle the influx.

Ready to Automate Your Accounts Receivables Processes?

Discover how embedding payments capabilities into your legacy software and ERP solutions can help your department reduce costs, improve productivity, enhance visibility, and mitigate potential fraud and compliance risks.