Making and receiving business-to-business (B2B) payments has long been seen as a problem.

It’s something that has stymied buyers and suppliers for years, and the operational disruption caused by the sudden shift to remote working arrangements has only complicated things.

22% of accounts payable leaders surveyed recently, by the Institute of Finance and Management (IOFM), say that it’s harder to pay suppliers on time when their staff works remotely.

Things aren’t any easier for suppliers. Half of accounts receivables leaders are less than satisfied with how their payments and receivables processes have worked during the pandemic.

All this begs the question - why B2B payments don’t seem to be getting any better, especially when you consider the C-Suite’s focus on reducing costs and improving cash flow in times like these.

Friction in the B2B payments lifecycle cannot be blamed solely on paper checks.

65% of businesses have increased their migration to electronic payment since last year.

Today, buyers and suppliers have access to more electronic payment options than ever, including Automated Clearing House (ACH), Real Time Payment (RTP), cards, wire transfer, and cross-border payments.

The reality is that friction in B2B payments is rooted in matters of systems integration.

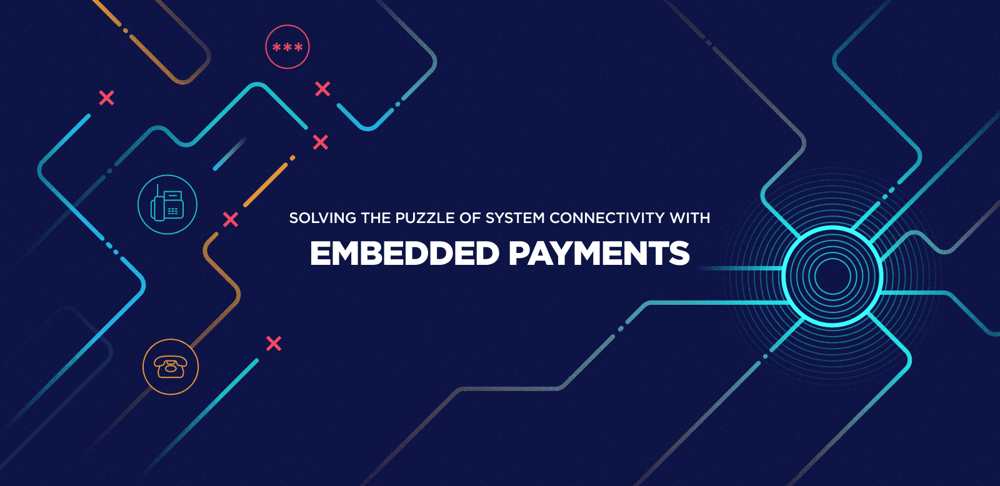

The Systems Connectivity Issue

One of the fundamental problems with B2B payments is the way that they have historically worked. The tendency has been for B2B payments to originate and be received using closed loop systems at different points across the supply chain, such as in accounts payable and accounts receivable.

Each of these systems requires its own logins and passwords, account requirements, file formats, and proprietary integrations. The result is inefficient and error-prone communications such as:

❌ paper checks and remittances

❌ e-mail and faxes

❌ phone calls

❌ portals

❌ electronic data interchange (EDI)

More significant than the disjointed processes, however, is the fragmented data accessibility and visibility that accompanies the silo approach that most businesses take to payments. Considerable volumes of payments data is held in standalone systems.

The problems with poor integration across the B2B payments lifecycle is reflected in the huge among of manual keying, paper shuffling and chasing down of information that occurs across the procure-to-pay and order-to-cash lifecycles.

Businesses have unsuccessfully tried to bridge the gap between their B2B payments systems and ERP applications and other software through manual inputs, file uploads, and complex integrations.

But getting things working together is nearly impossible in this type of environment. A prime example is the weak treasury connectivity that most businesses have struggled with for years.

It’s for this reason that buyers and suppliers have not solved the perennial challenges of B2B payments. By embedding B2B payments into their ERP applications and other software solutions, however, buyers and suppliers are able to finally achieve the vision of frictionless commerce.

Data and Payment Connectivity

Embedded payment solutions use ERP and bank connectors to facilitate the seamless, electronic flow of payments and related information from within any ERP platform or line-of-business software.

The technology’s multi-rail capabilities make it easy for buyers and suppliers to disburse or receive payments in any format. Payments also can be initiated or received via a business network of buyers and suppliers. Payments can be sent or received instantly or scheduled in advance to one or more suppliers within a buyer’s ERP platform.

Embedded solutions ensure that payments are made in a supplier’s preferred format and comply with the supplier’s payment terms maintained in the ERP. And rich remittance details flow electronically with payments, allowing for real-time reconciliation and the elimination of the manual tasks that burden accounts receivable and accounts payable staff.

A built-in centralized business directly streamlines the onboarding of suppliers.

By embedding payments into an ERP application or other software, buyers and suppliers can:

![]() Digitize and simplify invoice and payments processing

Digitize and simplify invoice and payments processing

![]() Automate payment and data reconciliation

Automate payment and data reconciliation

![]() Enhance cash management with better predictability

Enhance cash management with better predictability

![]() Reduce order and pricing discrepancies

Reduce order and pricing discrepancies

![]() Achieve end-to-end visibility and better treasury connectivity

Achieve end-to-end visibility and better treasury connectivity

![]() Strengthen risk controls

Strengthen risk controls

None of this is possible when B2B payments operate standalone from ERPs and other software.

A Smart Approach to Payments Integration

If your business is looking for ways to improve data and payment connectivity -

Transcard wants to speak with you.