If managing your receivables seems harder these days, you are not alone.

Why Are Accounts Receivables Increasingly Complex?

Processing customer receivables is more complex in four ways:

1. New Payment Types

1. New Payment Types

Paper checks are losing their grip on business-to-business payments.

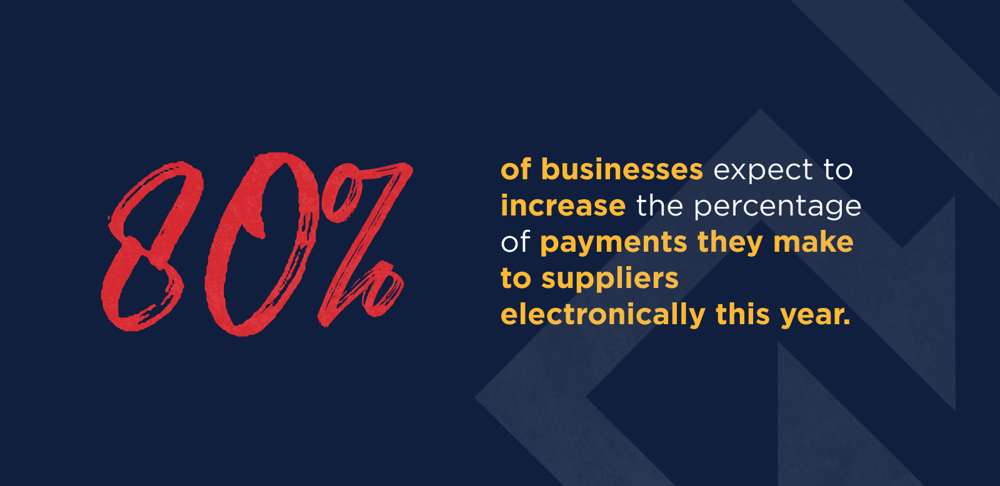

In fact, according to the Institute of Finance and Management:

IOFM also predicts that a majority of businesses will soon make more payments to suppliers using Automated Clearing House (ACH) transactions, rather than paper checks.

In addition to that, accounts payable departments are now embracing cards, PayPal and other payment methods for transactions.

Although new payment modalities are seemingly being introduced at an accelerated rate, many suppliers operate standalone systems to process each payment type that they support.

Maintaining multiple payment systems increases overhead, burdens IT, and results in payment silos.

2. More Payment Channels

2. More Payment Channels

“Do more with less” is the mantra in most businesses these days.

Consolidating systems used to support proliferating payment channels is a good place for accounts receivables leaders to start.

Most accounts receivable departments operate with point solutions for each way that they receive payments:

-

in-person (e.g., walk-up location)

-

point of sale (POS)

-

interactive voice response (IVR)

-

automated teller machine (ATM) or kiosk

-

the Internet, through a mobile device, and via file transfer.

Each of these systems has unique logins and passwords, account requirements, file formats, and proprietary integrations resulting in inefficient and unnecessarily complex processes.

3. Increasing Demand for Real-Time Visibility of Receivables Data

3. Increasing Demand for Real-Time Visibility of Receivables Data

Real-time cash flow visibility can be increasingly crucial in turbulent times.

Knowing exactly where things stand at any point in time helps inform strategic decisions and enables managers to better focus their collections efforts.

Legacy receivable solutions often make it difficult for accounts receivable leaders and others to access the timely insights that they need.

Remittance data frequently arrives separate from payments and often includes:

-

inaccurate & untimely data

-

poorly integrated systems

-

information needing to be rekeyed

All this is despite the millions of dollars that many businesses have invested in world-class enterprise resource planning (ERP) applications.

4. More Compliance and Security Pressure

4. More Compliance and Security Pressure

The stakes have never been higher for businesses to manage their receivables data in a compliant and secure manner.

The handling of receivables information is governed by an ever-increasing pile of regulations and rules, including:

-

Know Your Customer

-

Anti-Money Laundering (AML) laws

-

Regulation E

-

Regulation CC

-

Check 21

-

Uniform Commercial Code (UCC)

-

Office of Foreign Asset Controls (OFAC), and more.

Additionally, law enforcement agencies warn that payments are increasingly more at risk to fraudsters due to the operational disruption caused by the sudden shift to remote working.

Why Automate Accounts Receivable with an A2A Solution

Legacy receivables systems and processes aren’t enough to meet these significant challenges, while outsourcing receivables to a lockbox provider is typically a costly half-measure.

Businesses need a fresh approach to managing receivables.

They need an Account-to-Account (A2A) solution.

Unlike traditional receivables systems, an A2A solution digitally connects buyers and suppliers through their banks and ERP applications.

Integrating an A2A payments solution with a legacy ERP enables remittance information to be uploaded without human operator intervention, increased cash application speed, and zero operational inefficiencies.

Leading A2A solutions also include a centralized business directory that streamlines supplier onboarding, manages supplier payment terms and preferences, provides an additional measure of security, and facilitates real-time payments visibility.

An A2A payments solution uniquely addresses the challenges that receivables departments face:

-

Omni channel capabilities support any payment type.

-

Multi-rail functionality enables payments through any channel.

-

Rich remittance data flows electronically for touch-free posting.

-

A business directory and bank-grade security keep suppliers compliant and their data safe.

If your receivables processes are complicated, Transcard may have a solution.

Let’s arrange a time to chat about how our A2A solution can help.