Everything in the business world is moving faster these days.

Everything, that is, except commerce between buyers and sellers.

The Reality of Business Payments

Business-to-business commerce is bogged down by inefficient, unnecessarily complex, and risky payment processes. Friction in the way that businesses pay and get paid increases operational overhead, wastes employee time, impairs reporting, and contributes in a big way to late payments.

Not surprisingly, more treasurers are looking for ways to achieve frictionless payments.

The maturation of solutions incorporating real-time payments (RTP) will create an opportunity in 2021 for financial institutions of all sizes to help their corporate clients significantly reduce the amount of friction in their B2B payments while accelerating the flow of funds in the process.

The result of strong customer demand for a ubiquitous payment solution that is faster, smarter, and more secure than traditional B2B methods such as checks and Automated Clearing House (ACH) payments, RTP clears and settles transactions between accounts at financial institutions in real time.

Unlike checks and ACH, RTP does not rely on batched or delayed payments and is available 24/7.

What is more, B2B solutions that incorporate RTP can facilitate the exchange of remittance data, eliminating the need for payers to send a separate costly and error-prone remittance advice.

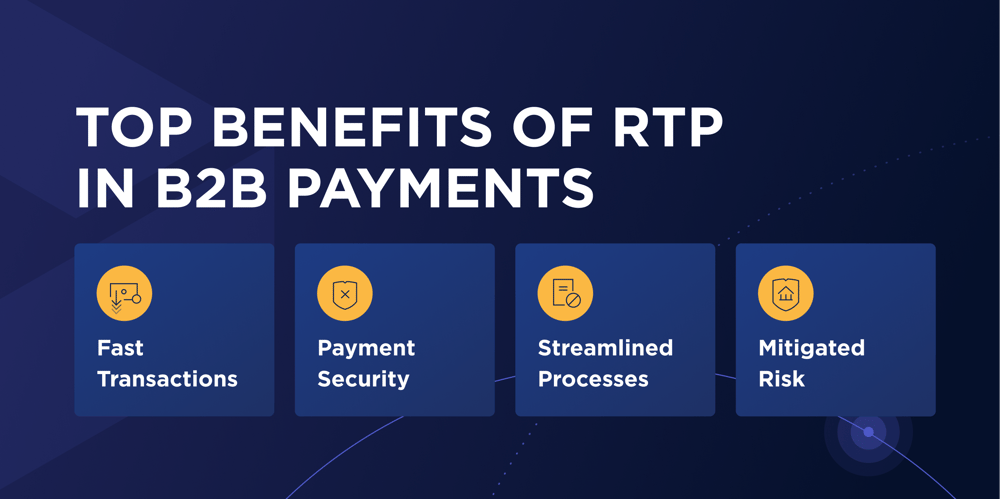

The 4 Top Benefits of RTP in B2B Payments

RTP solutions will help businesses forget everything they know about B2B payments.

1. B2B payments made via RTP are fast.

Imagine taking delivery of a shipment on your dock, effortlessly approving an invoice sent to a tablet or smartphone and triggering a payment that is made to your supplier within seconds – or whenever you want it scheduled – without the need for paper handling, manual data entry, and chasing down billing information.

Solutions that incorporate RTP make this possible, delivering financial and operational benefits.

2. B2B payments made via RTP are irrevocable.

No more pending payments or debits. No incomplete payments. No payments “lost in the mail.” Payers know within seconds whether a payment was successful, eliminating the need to call their bank to check on the status of pending transactions. And prefunding RTP accounts reduces the possibility of overdrafts.

All this provides big efficiency gains for payers and banks. Suppliers benefit from better cash flow certainty and less need to call or e-mail clients to check on the status of payments.

3. Streamlined accounts payable and accounts receivable processes.

Attaching rich remittance data and other messages to payments eliminates the need for payables staff to generate and manage separate remittance advices for each payment.

Receiving electronic remittance data that can be posted directly to an enterprise resource planning (ERP) application provides suppliers with faster cash application, enhanced cash flow forecasting, and big operational savings from the elimination of matching and posting payments and remittance advices.

4. Less risk.

Global law enforcement entities are sounding the alarm that fraud is on the rise. With traditional B2B payment methods, buyers can never be sure that the entity they are paying is who they proport to be.

Solutions that leverage RTP mitigate these risks by leveraging hardened payment infrastructure that incorporates an online centralized directory of businesses, reducing the possibility of losses from phishing attacks and other schemes.

How RTP Solutions Help Transform the Customer Experience

It is not just businesses that stand to benefit from bank payment solutions that incorporate RTP. The ability for near-instantaneous transfers between financial institutions also has great applicability for peer-to-peer (P2P), business-to-consumer (B2C) and consumer-to-business (C2B) transactions.

Solutions that incorporate RTP offer tantalizing possibilities for disbursements in the insurance and mortgage industries.

Integrated bill-pay services in the C2B space will enable consumers to manage their bills in real-time. And RTP may become a way for consumers to make P2P transfers.

The possibilities of how banks can enhance their customer experience with RTP are endless. The technology gives banks a chance to take a fresh look at how they approach payments services, and to better align their portfolio of payments solutions with the needs of target industries and segments.

Accelerating B2B payments with solutions that incorporate RTP are a good starting point for banks.

Banks Primed to Leverage RTP in 2021

Banks that take the lead on frictionless payments stand to gain higher customer satisfaction, reduced client attrition, and lower costs.

For instance, migrating from batch processing to real-time payments offers an enhanced customer experience. And just think of the money a bank can save by weaning its business clients off paper checks. This is music to a bank executive’s ears in tough times like these.

There also is the possibility that RTP can result in lucrative new revenue streams for banks.

All this will result in a competitive edge for banks that embrace B2B solutions that include RTP.

Banks that drag their feet on RTP may soon find themselves a competitive disadvantage.

74% of financial institutions are implementing or considering implementing RTP across at least one of their customer segments, according to survey conducted by Levvel Research.

What is more, 17 percent of banks have gone live with RTP across all their customer segments. Only three percent of banks are not planning to adopt RTP in any customer segment, per Levvel Research.

These banks believe that RTP will benefit their customers while providing their bank with an edge.

Is your bank ready to capitalize on RTP? If so, Transcard wants to speak with you.