CFOs intuitively know that the way their business makes and receives payments is inefficient.

But most CFOs do not realize the extent of the problem.

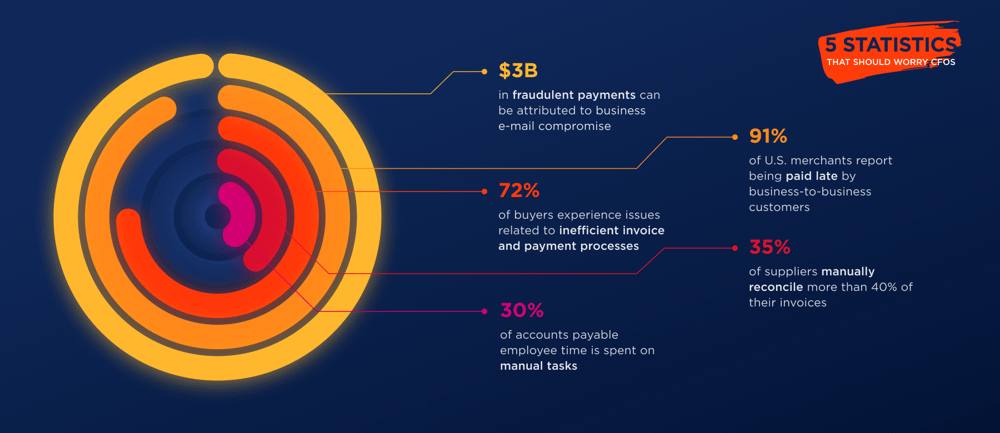

Here are five statistics that should be a wakeup call for CFOs:

91% of U.S. merchants report being paid late by business-to-business customers [1].

72% of buyers experience issues related to inefficient invoice and payment processes [2].

30% of accounts payable employee time is spent on manual tasks [3].

35% of suppliers manually reconcile more than 40 percent of their invoices [4].

$3 billion in fraudulent payments can be attributed to business e-mail compromise [5].

These sobering statistics leave no room for doubt: the friction from outdated, inefficient business-to-business payment processes are negatively impacting critical metrics such as operating costs, Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO).

With 22 trillion business-to-business payments made in North America each year [6], these problems cannot be allowed to fester.

Here is what CFOs need to do modernize their business-to-business payments flow:

Streamline Processes

Friction in making or processing business-to-business payments can stunt, or even stop, business growth. The longer it takes to process and post a payment, the longer a business has outstanding costs. Delays in processing payments can unnecessarily hold up the delivery of goods and services, strain customer relationships, disrupt cashflow, and hurt a supplier’s reputation.

Delayed payments can even put a business in jeopardy. Real-time payments (RTP) accelerate the receipt and posting of payments while providing assurance that payments will be received on time. RTP transactions are irrevocable.

Become Data Rich

Most payments do not arrive with the data that suppliers need for reconciliation. As a result, accounts receivable professionals waste a lot of time chasing down information, resolving exceptions, and rekeying data. Making matters worse, many businesses rely on spreadsheet to manage payment terms and reconcile transactions.

It is no wonder that manual processes are the top challenge for 60 percent of treasury professionals [7].

What if the right data always arrived with a payment? Real-time data exchanges make this possible by putting business-critical information into a supplier’s hands with every payment.

Think Connectivity

Much of the cost and complexity of business-to-business payments can be traced to the disconnected systems, processes, and standards that businesses use to make and receive payments. Business-to-business payments can originate at numerous points across the supply chain.

Closed loop networks and bilateral integration limit automation. And multiple logins and passwords, account requirements, file formats, and proprietary integrations must be managed. Buyers and sellers need a way to systematically connect to each other through their ERPs and share payment data using common rules and standards.

Safeguard your Payments

Twenty-five percent of accounts payable professionals fear that the way they are doing things these days is creating new fraud and compliance risks. Old approaches to storing supplier banking details and making and receiving payments throw the door open wide to fraudsters (Exhibit A: business e-mail compromise).

Using a centralized business directory is critical to helping improve security. Enrolled businesses receive a unique ID to safeguard sensitive bank account details and to codify counterparties.

With a central business directly, trading partners no longer need to share and store bank account details for payments, buyers can always be sure that they are paying the right counterparty.

If fast, transparent, and secure business-to-business payments workflows sound enticing, here is the good news: a new breed of account-to-account payment solutions will radically transform the way businesses make and receive payments. The solutions will digitally connect buyers and suppliers through their banks and ERP platforms to facilitate frictionless business-to-business commerce.

Eliminating the friction from business-to-business commerce will benefit buyers and suppliers:

- Buyers will achieve better working capital, improved data quality, and increased security.

- Suppliers will gain more control over their cashflow, greater efficiency, and less risk.

All this will result in a modern, frictionless business-to-business ecosystem. If your business is ready to modernize the way it does business, Transcard wants to speak with you.