Managing payments and the associated data is at the core of every business process.

Customer receipts and supplier disbursements must be recorded and satisfied with a payment. But the way that businesses make and receive payments is complex, time-consuming, costly, and risky.

Banks have a unique opportunity to do something about this.

B2B Payment Challenges

Outdated, inefficient processes are still the norm in business-to-business (B2B) payments.

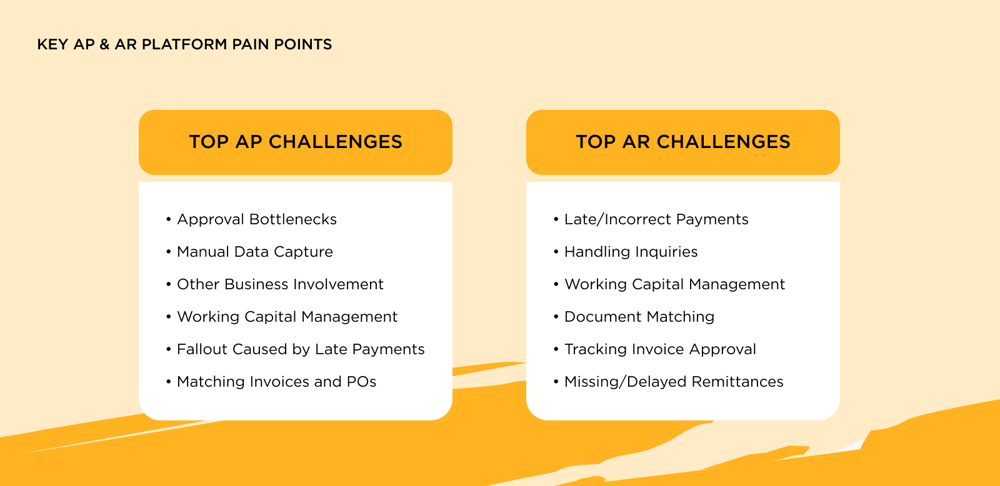

For starters, businesses of all sizes use spreadsheets to manage payment terms and manually reconcile invoices. Accounts payable employees waste lots of time on manual tasks such as data entry, paper shuffling, and chasing down information.

Accounts receivable departments must contend with multiple payment and data silos. Juggling disparate payment channels also is a big headache for accounts receivable leaders. And nearly half of all invoices that suppliers issue are manually reconciled.

Supply chain managers must manage delivery delays and strained supplier relationships caused by inefficient invoice and payment processing. What’s more, payment fraud is a problem that is exacerbated by poor visibility and controls in the B2B commerce lifecycle.

Friction in the B2B lifecycle takes a big toll on businesses. Issuing and depositing checks costs U.S. businesses $26 billion annually. Additionally, businesses lose billions annually in check fraud.

And inefficiencies in making payments is a big reason that 91% of B2B merchants in the United States reported late payments by their customers.

In fact, 50,000 small and mid-sized businesses fail each year in the United States due in part to late payments from customers.

There is no question that cash flow shortfalls can stunt, or even prevent business growth.

Many businesses turn to financing to smooth out dips in cash flow. But financing solutions can be pricey. And they are not always easily accessible to small or mid-sized businesses.

Clearly the way that businesses pay and get paid isn’t good enough.

How Banks Can Streamline B2B Payments

Paper checks are a big part of the friction in B2B payments.

While consumers have largely ditched paper checks in favor of electronic alternatives, checks still represent a significant percentage of B2B payments.

Most accounts payable departments still make some portion of their supplier payments using a paper check.

The smaller the business, the higher the percentage of payments they are likely to make via paper check, payment studies show.

But checks aren’t the only reason for friction in B2B payments. Point solutions also play a role.

B2B payments originate at different points of across the supply chain. Each of these points may have their own closed-loop networks and bilateral integration, each with unique logins and passwords, account requirements, file formats, and proprietary integrations.

The result is lots of payment and data silos that contribute to back-and-forth phone calls, e-mails and faxes, limited remittance details, and employee time wasted keying data, shuffling paper, and chasing down financial information.

Low quality remittance data also is big problem in B2B payments.

Accounts receivable departments key, or pay a third-party to key, the remittance data required for cash application. And receivables staff waste lots of time chasing down remittance data or matching data to payments sent separately.

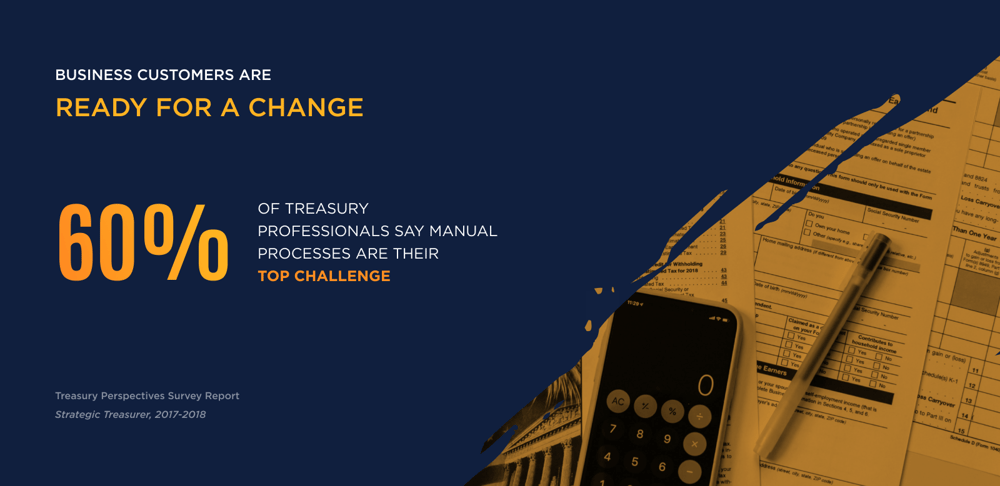

Treasury professionals recognize the problems with making and receiving B2B payments. Sixty percent of them say manual financial processes are their top challenge. And studies show that corporate finance leaders are inclined to turn to their banks for B2B payments solutions.

What is an A2A solution?

Banks can help their business customers address the challenges of B2B commerce by extending their payment services portfolio to include automated account-to-account (A2A) solutions.

A2A solutions make it easy for business to pay and get paid. The technology systematically connects buyers and suppliers to each other to share payments and data using common rules and standards.

Among other benefits, A2A supports multiple payment rails, enables the passage of remittance data, reduces late payments and lowers operating headaches and risks for buyers and suppliers.

This is a game changer in B2B payments.

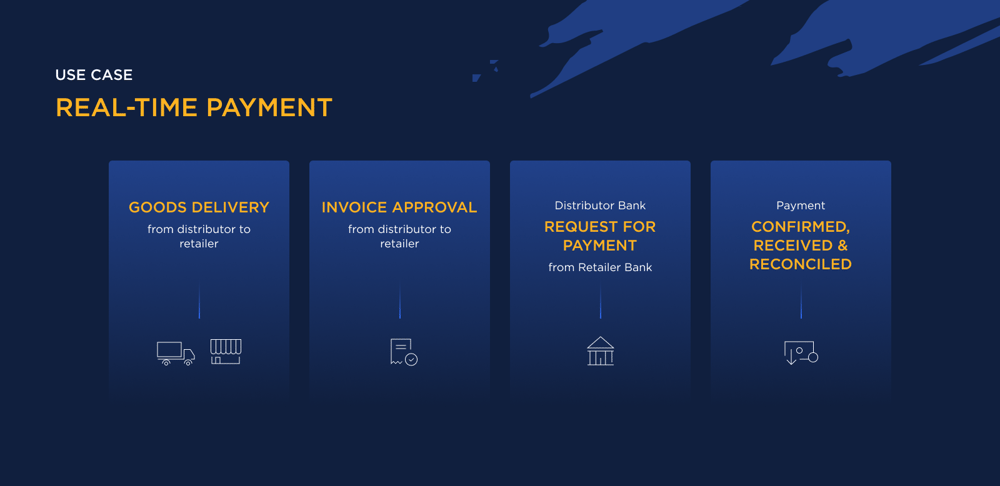

A2A solutions combine electronic payments functionality, such as Real-Time Payments (RTP) with:

- accounts payable and accounts receivable invoicing;

- ERP integration; and

- payment services onto a single solution.

The RTP network facilitates the immediate transmission and settlement of payments and the exchange of standardized and enhanced remittance data.

Invoicing capabilities enable suppliers to instantly present invoices via an e-invoice 24/7/365 for initial or recurring bills via a customer’s preferred online or mobile banking channel.

Seamless ERP integration connects buyers and sellers and facilitates the exchange of data without the burden of a costly and resource-intensive project.

Rich, real-time data exchanges streamline payment reconciliation. And payment services manage a directory of trading partners, payment terms and preferences, standard reconciliation information, and banking accounts details. The information typically required to send electronic payments (the bank routing number and account number) is not always readily available.

Payment services remove this barrier to electronic payments adoption. An A2A automation gives businesses the ability to automate payments without the need to share or store sensitive bank account information.

Eliminating friction in the B2B lifecycle has big implications for banks. A2A automation adds revenue, lowers costs and improves the customer experience.

By providing a better level of service for customers, banks can expect more and/or new revenue on carded and non-carded transactions.

The B2B capabilities in an A2A solution also can help drive RTP volume. With an A2A solution, it is easier for banks to onboard suppliers. And it is cheaper for banks to process payments on behalf of their business clients.

Importantly, A2A helps banks stand out in a crowded market and helps answer the challenge posed by fintechs encroaching on bank payment revenues. Banks can deliver more value to their customers by cross-selling services with the new data received for each payment.

How Banks Can Seize the A2A Opportunity

With a lot riding on B2B commerce, buyers and sellers are looking for ways to improve the efficiency and effectiveness of their payments processes through modernization.

Now is the time for banks to rethink the role they play in business-to-business commerce.

Bank lockbox services are no longer enough. Treasurers for both large corporations and small businesses are looking for payments automation solution. Many are turning to fintechs for help. But most of these fintechs are focused on card-based solutions that only solve part of the problem.

Deploying an A2A solution is worth the investment for banks. Payments hold valuable data that can fuel innovative new products and help banks generate new revenue and tighten client relationships.

Lean how your bank can make frictionless payments a reality for its clients.

Click here to watch the full Transcard webinar on how banks can benefit from A2A.