Remember when paying suppliers and individual meant cutting checks?

Today, businesses disburse funds using a growing mix of payment types and payment rails.

And more.

Few people would argue that disbursing paper checks is better than these electronic alternatives.

But managing all the methods for paying suppliers and individuals is not easy for most businesses, banks, and fintechs. Juggling single and mass payments and ensuring the suppliers are paid on-time, per their payment terms, further complicates things for businesses, banks and fintechs.

Reconciling all these payment types can be a laborious, time-consuming, and error-prone affair. The result, the process of disbursing payments typically is inefficient, unnecessarily complex & risky.

Blame the hodgepodge of point solutions and closed-loop networks that most businesses, banks, and fintechs use to disburse funds. Each of these point solutions and closed-loop networks require unique logins and passwords, file formats, user requirements, and proprietary integrations.

PriceWaterhouseCoopers estimates that roughly one-quarter of an accounts payable professional’s time is wasted on tasks that should be automated.

Not surprisingly, finance executives surveyed by the Institute of Finance and Management (IOFM) rank accounts payable as the most labor-intensive and paper-intensive finance and administration function, and the task that would benefit most from automation – which is really saying something when you consider other laborious finance functions.

Banks. Things aren’t much better for the banks that serve businesses. Most banks rely on siloed systems for making payments on behalf on their business systems. Banks must spend big bucks helping some business clients integrate various payment feeds into their ERPs and core financial systems.

Businesses. Other businesses must reconcile bank statements for each channel through which they pay suppliers and individuals. In many cases, switching suppliers or individuals from one bank payment channel to another is a hassle that involves lots of paperwork and a long and complicated onboarding process.

Fintechs. For their part, fintechs must invest significant time and money incorporating various payment streams into their solutions – resources that could be better spent on their core product capabilities. And fintechs must find ways to keep their payments capabilities up to date and secure.

Businesses, banks, and fintechs will never eliminate the friction in disbursing payments until they more seamlessly connect payment systems with legacy ERPs, software applications, and API layers.

Strategies for Streamlining Disbursements

New technology is providing businesses, banks, and fintechs with a smarter way to disburse funds.

Here are three things to look for in a solution that are sure to help streamline disbursements:

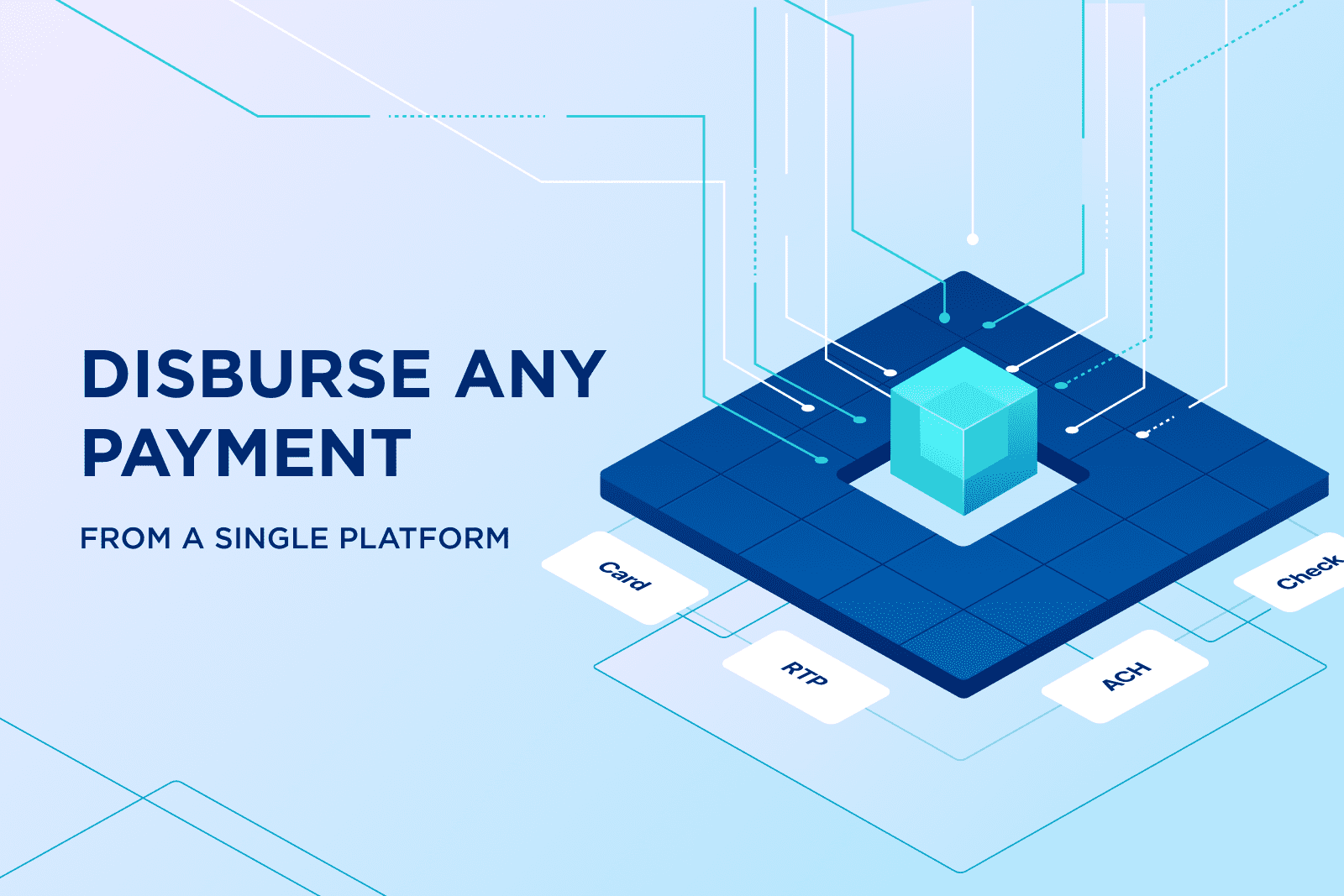

Multi-Rail Payment Capabilities

Forcing suppliers and individuals to accept the payment method that works best for your business is no way to build strong relationships. Suppliers and individuals may have strong preferences for how and when they would like to be paid. But supporting a wide range of standalone payment systems can be a big burden on an AP department.

Find a disbursements solution that makes it easy to execute single or mass payments, in any payment method, using any payment rail. Look for a solution that allows you to make payments in real-time or schedule them for later.

Some solutions enable users to define rules for how suppliers or individuals should be paid. Others keep track of existing payment terms to ensure that payments are made on time.

TIP: Ensure that the solutions provider has a track record of embracing new payment methods and payment rails.

Seamless Integration

A lot of the friction in the commerce lifecycle can be traced back to poorly integrated systems.

Eliminate this inefficiency by deploying a disbursements solution that seamlessly connects with any legacy ERP platform, software application, or bank API layer.

Determine whether a technology provider offers open APIs, pre-integrated systems, or connectors to bank API layers. Some technology providers have direct connections with dozens of leading ERP platforms. With a tightly integrated disbursements solution, accounts payable staff can make payments from directly within the familiar screens of their legacy ERP or software application, using drop-down menus and a few clicks of the mouse.

Auto Reconciliation

IOFM estimates that 84% of an AP practitioner’s day is spent keying data, shuffling paper, and chasing down information – time that could be better spent on higher value activities such as analyzing data, collaborating with stakeholders, building relationships with suppliers,

reconciling payments to suppliers & individuals.

By tightly integrating a payment solution with a legacy ERP or software application, data can be reconciled automatically, in real time.

Finding a solution with these three attributes provides businesses, banks, and fintechs with greater flexibility and control in paying suppliers and individuals, all from a single innovative platform.

Learn how we are helping businesses, banks, and fintechs take a smarter approach to disbursements.