A rapidly evolving Banking-as-a-Service (BaaS) market is starting to take shape.

A BaaS platform enables fintechs and other third parties – as well as banks and credit unions – to connect with licensed and regulated banking back-ends via Application Programming Interfaces (APIs) so they can build financial services applications.

In some cases, the banking back-ends are provided by fintechs that offer a BaaS platform and deliver core banking services at the same time.

The near-term dynamics of the BaaS market are potent, driven by strong customer sentiment, a thriving fintech environment, and unrelenting innovation by providers of BaaS platforms.

Fintechs already are leveraging BaaS platforms for:

- The issuance of bank accounts and cards

- Expense management

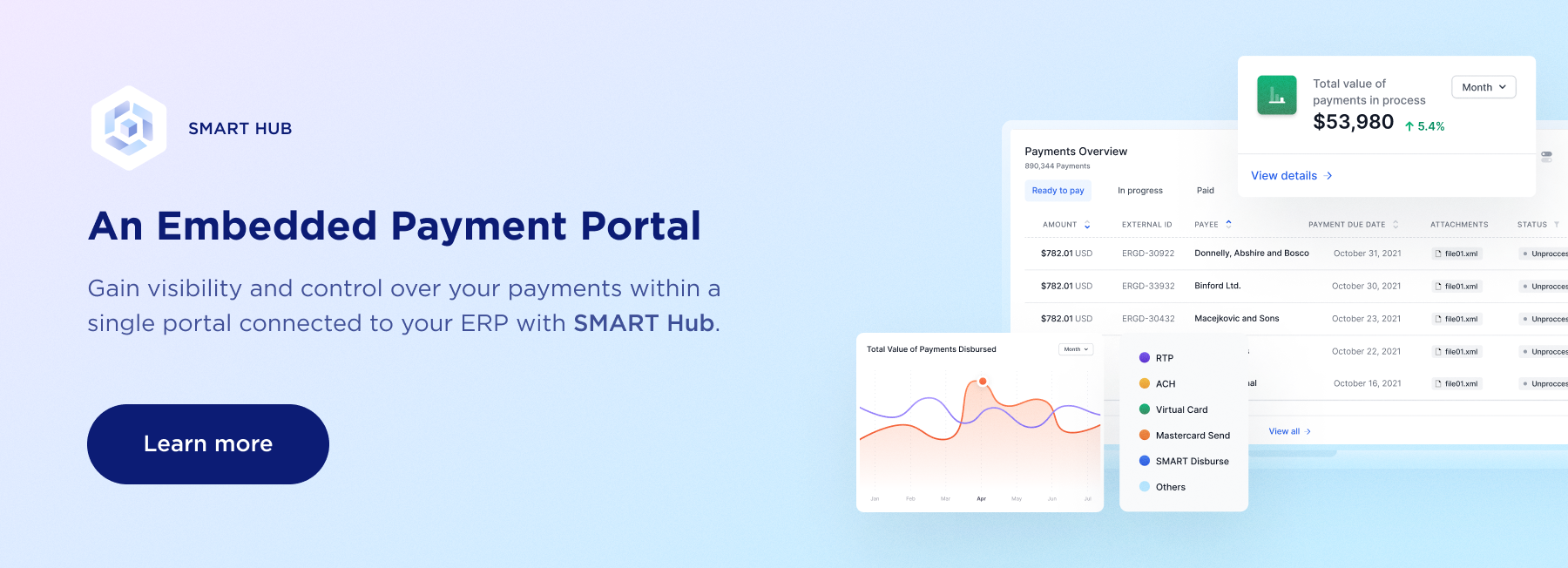

- Applications that require customer funds to stay separate

- The management of sub-merchant accounts

- Creating mobile e-wallets

- Supporting marketplaces for consumer and merchant accounts

Looking further into the future there are seven trends that will impact BaaS:

Real-Time Processing

Everything moves faster these days. That is why BaaS platforms will continue to move towards real-time payment processing. Traditional core banking platforms are built around antiquated batch processes, which make settling the electronic payments made by consumers far from simple.

Most payment services providers will transfer bulk sums of money into a biller’s bank account. The bulk sum represents payments made on all outstanding invoices, as well as the acquirer’s fees. Separating the acquirer’s fees, reconciling payments and invoices and updating the general ledger can become laborious and time-consuming.

Poor visibility into payments also opens the door to compliance issues. And some traditional batch-mode solutions do not support all electronic payment methods. It is for these reasons that fintechs will expect BaaS platforms to support real-time processing.

Omni-Channel Payments

Traditional core banking platforms have been slow to support newer payment methods. But customers demand choice in how they make and receive payments. That is why omni-channel payment processing is becoming the table stakes for BaaS platform providers.

An omni-channel BaaS platform enables consumers to make and receive payments electronically via their preferred method, whether it is via card, Automated Clearing House (ACH) or Real-Time Payment (RTP). All payments are aggregated onto a single BaaS platform for processing and settlement.

The BaaS platform then provides granular visibility into individual payments as well as complete transparency and tracking of consumer payments from receipt through settlement, without the need for pricey customized reporting engines.

All this offers a better, more flexible way to manage payments.

Digital Onboarding

Digital onboarding raced up the priority list in financial services with the dramatic shift to remote work. With no end in sight to this new abnormal, fintechs must carefully review their digital plans to ensure they have the capabilities they need to digitally onboard customers across markets, products, and segments. BaaS can help.

Leading BaaS platforms incorporate digital onboarding capabilities that are proven to free up staff time, accelerate turnaround, slash costs, reduce errors, and enhance the onboarding experience.

Data Monetization

The insights generated from core banking data can open a host of online applications with the potential to develop vast new markets. For business customers, this might mean easy access through fintechs to information for managing cashflow, utilities, insurance, payroll, and real estate.

Multi-service consumer platforms may leverage core banking data for applications such as insurance, utilities, entertainment, and travel.

Smarter Technologies

Artificial intelligence (AI) and other cognitive technologies will soon raise the bar for operational efficiency and effectiveness by performing tasks in core banking that previously required human judgement. Incorporating AI into a BaaS platform automates the gathering and analysis of data, preparation and display of information, identification of trends and anomalies, and the presentation of a recommended course of action.

Industry Focused Applications

BaaS will empower industry-specific applications that will change the way the consumers and businesses think about conducting financial transactions. BaaS-powered applications already have emerged in healthcare and gaming, for example.

It is only a matter of time before BaaS gains critical mass among fintechs in the United States.

Longer-term, BaaS will further evolve to deliver applications that are even more flexible and robust.

For more information on how Banking-as-a-Service is set to impact the next generation of fintech products, check the executive insights report in the

playbook co-sponsored by Transcard & PYMNTS